English

English

Deutsch

Deutsch

Español

Español

Français

Français

Português

Português

日本

日本

한국인

한국인

Türkçe

Türkçe

Русский

Русский

Tiếng Việt

Tiếng Việt

Volatility Trends

Crypto assets have a reputation for extreme volatility, but the nature of this volatility is more nuanced than just wild and unpredictable price swings. While major crypto price moves are often larger compared to other asset classes, they typically follow extended periods of relatively low volatility. The bear market we find ourselves in has seen this cycle multiple times, with volatility spikes induced by events like the FTX collapse or SVB bank failure. This dynamic creates an exciting playing field for options traders, requiring strategies for profiting in low-volatility environments and breakouts.

Recent market history of BTC and ETH has produced another example of this “slowly then all at once” volatility dynamic, as spot prices hovered in place during June and July before a sharp 10% decline in August. With this recognizable pattern in hand, here are a handful of options strategies for playing low volatility and price spikes.

BTC price plateaued from late June to mid-August

Low Volatility

Before the August 16th spike, BTC volatility had been trending steadily downwards since late June. The options market was ripe for selling volatility and collecting premiums during this period.

BVOL 7-day historical BTC volatility index

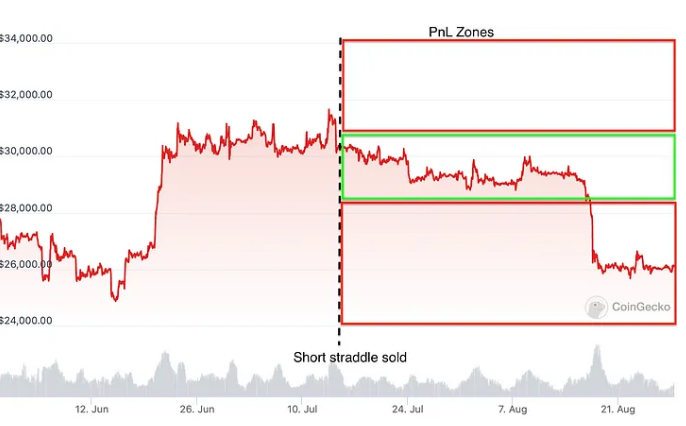

Short Strangles and Straddles are valuable strategies to employ in this type of scenario, especially considering that BTC implied volatility has historically been higher than realized volatility. Since short strangles and straddles both involve the sale of a put and a call, exacerbated IV presents an opportunity where the contracts may be overpriced, increasing premiums to earn if they expire out of the money. These strategies are bets on mean reversion of volatility between big moves, which historical BTC data supports.

Short straddles are the more aggressive of the two strategies since traders sell both contracts ATM. Higher premiums are available here, but breakevens are going to be tighter. Since strangles use OTM contracts, there’s more room for price movement before losing money, but premiums will be lower. In this specific timeframe from mid-June to mid-August, straddles would have been the more profitable choice, considering the extremely low realized volatility. Ultimately, either strategy would’ve been a solid win, so preference comes down to risk tolerance.

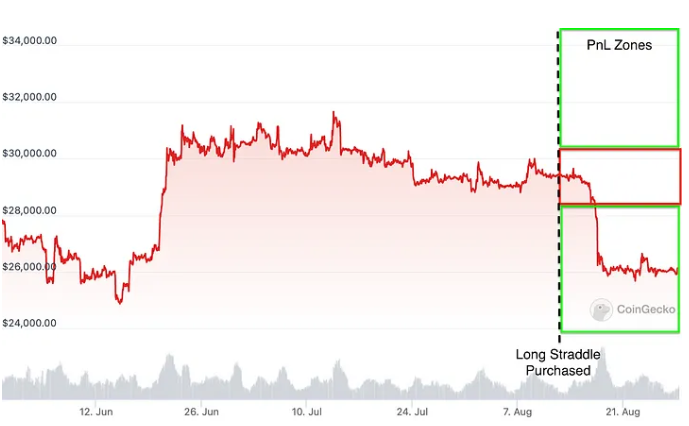

PnL zones for a hypothetical short straddle

Enhanced Yield with ETH Staking + Call Selling

Another strategy that has gained popularity in recent low-volatility periods is staking ETH while selling ETH calls to produce a boosted yield (premiums + staking rewards). From a risk standpoint, the calls are “covered” since the seller also owns the underlying asset, an element of the strategy made possible by the April 2023 Shanghai upgrade that enabled unstaking. Staking yield is typically ~4%, varying slightly by platform, and adding short volatility exposure on top via call selling can work nicely for a longer-term accumulation strategy.

PnL zones for a hypothetical call selling strategy

Stack up more ETH through premiums and staking rewards, roll those into staked ETH to increase yield generating base, and even employ the LSD tokens received elsewhere in DeFi to increase yield further. This strategy combination unique to Ether will involve navigating multiple protocols. For example, stake ETH on Lido, sell calls on Siren, and then optionally LP stETH on Curve, Balancer, or a similar protocol.

Volatility Spikes

But what’s the options play when BTC or ETH look primed for a breakout? Maybe short volatility is getting too crowded, and squeeze potential is high, or there’s a key catalyst on the horizon that could swing the market. Many long volatility strategies can work here, with the primary considerations being risk tolerance and whether to take a directional bias.

Directional Exposure with Vertical Call Spreads

If a trader expects a breakout and is confident in the price’s direction, vertical call spreads are a common strategy. The breakout could follow the macro environment, expected regulatory decisions, or sentiment based on derivatives market flows. Whatever the reason, traders can tailor spreads to fit the direction of choice.

For the bull case, a trader will buy a lower strike call and then sell a higher strike call with the same expiration, referred to as a call debit spread. This trade gained some steam during recent months with expectations of a rally on the back of potential Bitcoin ETF approval. Unfortunately for those traders, August brought the opposite — a double-digit single-day drop in spot price. In hindsight, bearish vertical spreads were the preferred strategy. To set up a bearish vertical call spread, invert the structure by selling the lower strike call and buying the higher one. Both approaches limit potential losses, and the offsetting contracts reduce collateral requirements.

PnL Zones for a hypothetical bearish spread

For spread traders, Siren Flow is your on-chain platform of choice, as the portfolio margin system takes offsetting contracts into account. In contrast, other DeFi options platforms use separate margin calculations for each leg of a strategy, a far less capital efficient method.

Delta Neutral Exposure with Long Strangles & Straddles

Strangles and straddles are valuable strategies for a directionally neutral approach to volatility. As discussed above, straddles offer higher risks and larger potential profits, while strangles offer a greater chance to make a smaller profit. The main difference between these strategies’ long and short versions is that the long version caps maximum loss while the short version does not. Also, traders pay premiums for longs and receive them for shorts. The high conviction play would have been a long straddle during the mid-August volatility spike, offering a greater relative payoff than the aforementioned vertical spreads.